Lumine Group is a strategic acquirer and developer of Vertical Market Software (VMS) businesses serving the Communications and Media industries. Originally a vertical within Constellation Software’s Volaris Operating Group, Lumine was branded in 2020 and spun out as a standalone entity in 2023. The company operates a high-quality, perpetual-ownership platform in two mission-critical markets characterised by high switching costs and low churn. Its model combines disciplined capital allocation, a decentralised structure, and a ‘buy-and-hold-forever’ philosophy- creating a durable compounding engine focused on niche segments and complex carve-outs where competition is limited.

The Nyland Operating System

Founder and CEO David Nyland was one of Constellation’s most effective capital allocators, consistently delivering returns well above its industry-leading average of 25%. Over the last decade, Nyland has institutionalised a global and scalable acquisition framework (adapted from the CSU playbook) that balances business unit autonomy with accountability, driving high founder retention and strong inbound deal flow. His disciplined, long-term approach prioritises intrinsic value over short-term optics, reinforcing Lumine’s reputation as a preferred acquirer.

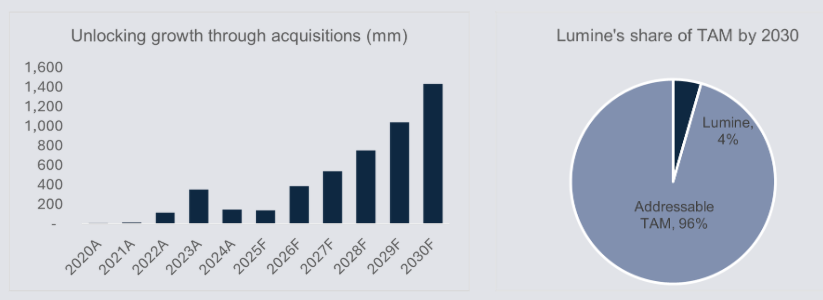

Large Addressable Market and Acquisition Runway

Lumine operates in the communications and media industries, with a combined $60bn M&A opportunity. The CEO reports a pipeline in the low thousands of targets, with active discussions in the hundreds. Current ownership of 33 businesses underscores significant future growth potential. As long-term investors, Lumine focuses on acquiring businesses with enduring growth potential, strengthening core profitability and making strategic investments to position them for sustained success.

Resilient Business Model

Lumine derives 73% of its revenue from recurring sources, up from 57% in 2020, reflecting a disciplined M&A strategy focused on mission-critical, subscription-based models. Post-acquisition, the ‘Lumine playbook’ enhances economics, prioritising recurring revenues and cash conversion, increasing reinvestment capacity. Combined with minimal leverage (<2× EBITDA) and robust margins (projected EBIT of 34.5% in 2025), the company maintains a durable and scalable model built for long-term growth.

Lumine’s Growth Engine: Disciplined M&A in a Vast Market

Source: Lumine filings, RBC, Ziller estimates1

Return Hurdles as Culture

Lumine applies a strict acquisition framework, purchasing businesses at 1–2× sales and 4–8× EBITDA, well below listed software peers. This approach delivers immediate 10–25% unlevered cash-on-cash returns, supported by a decade-long track record of strong performance. By avoiding reliance on financial engineering or multiple expansion, Lumine reinforces long-term value creation. The majority of the 33 acquisitions to date have met or exceeded >20% IRR hurdles. Furthermore, its reputation for respectful stewardship attracts sellers seeking continuity, helping to preserve key customer relationships.

Valuation & Return Profile

Lumine offers the highest forward revenue CAGR (>30%) among peers, minimal gearing, and a terminal PEG of 0.8×, supporting a >20% estimated total rate of return.