SpaceX is the defining company of the new space economy. Founded by Elon Musk in 2002 to make humanity multiplanetary, the company has transformed launch from a bespoke aerospace activity into a reusable, high-volume industrial platform. It now controls the core physical layers behind the next generation of space infrastructure; low-cost launch, satellite manufacturing, global connectivity, and increasingly (terrestrial) AI compute. In 2025, SpaceX completed 170 launches, carried 2,200 metric tons to orbit – more than the rest of the world combined – and represented more than 80% of all mass launched to orbit.

The Algorithm

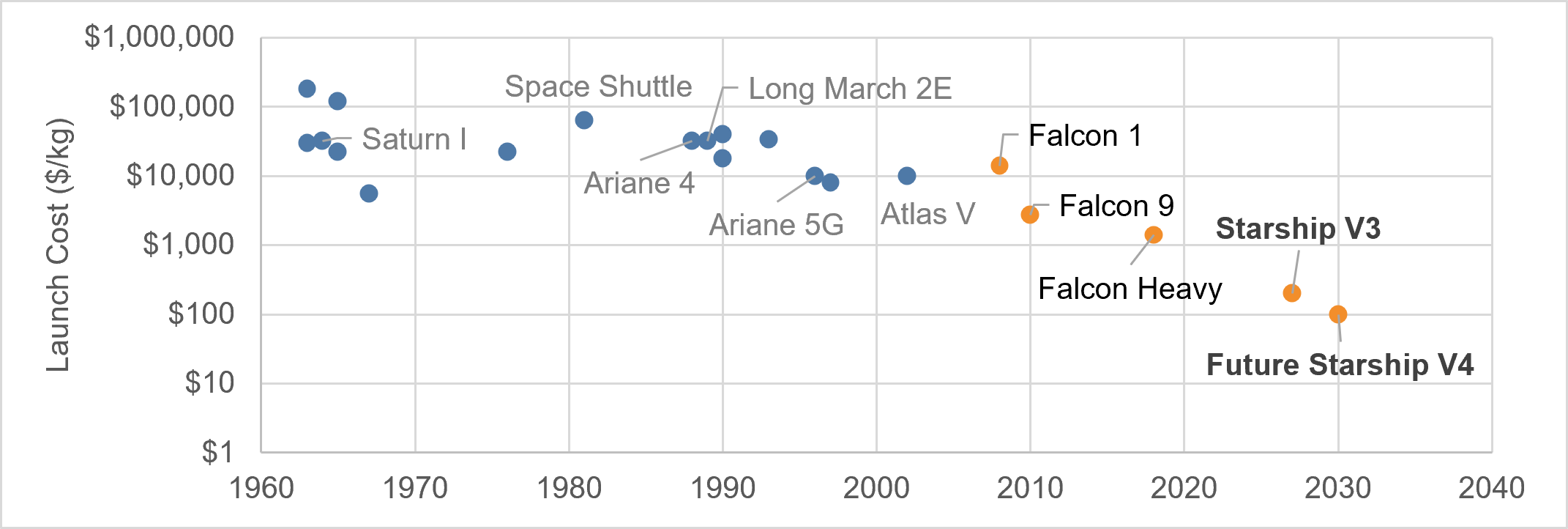

Elon Musk’s defining contribution has been to reframe aerospace through first-principles engineering and industrial scale. SpaceX was founded on the belief that rockets were expensive not because of physics alone, but because of inefficient processes, fragmented supply chains, and low-volume production. Musk’s response was to vertically integrate aggressively, simplify systems, iterate rapidly, and continuously compress cost curves. The company formalised this philosophy internally through “The Algorithm”: question requirements, delete unnecessary parts and processes, optimise only what remains, accelerate cycle time, and automate last.

Industrialisation of Space

Starlink is the clearest commercial proof of SpaceX’s launch advantage. It converts low-cost access to orbit into recurring revenue. On a scale unmatched, Starlink operates over 9,600 satellites and represented roughly 75% of all active maneuverable satellites in orbit. Starship, the largest and most powerful vehicle of any kind ever developed, is designed to carry over 100 metric tons to orbit in a fully reusable configuration, which will materially lower the cost of deploying satellites, communications infrastructure, and orbital compute.

Source: SpaceX and Ziller Funds Management | Constant 2021 $ per kilogram; plotted on a logarithmic axis

Orbit, Bandwidth and Compute

SpaceX is the only owner across all three scarce physical capacity – orbit, bandwidth, and compute. The company frames its long-term opportunity around a very large addressable market, estimating a quantifiable TAM at approximately $28.5tn, including $370bn in Space, $1.6tn in Connectivity, and $26.5tn in AI. Importantly, these markets reinforce one another. Launch enables satellites. Satellites enable global bandwidth. Bandwidth supports compute distribution. Distributed compute creates the next major infrastructure layer, AI.

SpaceX’s AI strategy is therefore an extension of the same playbook. AI growth is increasingly constrained by power, chips, and data centre construction. SpaceX’s “from shovels to tokens” approach attacks these bottlenecks directly by controlling physical infrastructure from power generation through to compute deployment. The Anthropic and Google agreement, under which SpaceX will provide access to COLOSSUS and COLOSSUS II capacity for $2.1bn per month through 2029, demonstrates that compute infrastructure is already monetisable at scale.

Valuation

The value of launch providers such as SpaceX and Rocket Lab has rallied substantially across public and private markets over the past few years. Ziller Global Fund has participated in this rally through our investment in Rocket Lab since late 2024. Given the elevated valuation at IPO, we chose not to participate in the SpaceX offering, but continue to monitor the stock closely for an attractive entry point.

SpaceX is expected to grow revenue by 81% in FY26, 61% in FY27, 49% in FY30, driven primarily by Starlink and terrestrial data centre monetisation. Our current Total Rate of Return estimate for SpaceX is approximately 10% p.a. over the next five years. Near term, the factors we are monitoring most closely are the pace of terrestrial data centre buildout, achieved compute rental rates, and progress in AI model monetisation (Cursor and broader enterprise adoption).